TMCR

****Sponsored by LFG Equities Corp and Disseminated on behalf of The Metals Royalty Company Inc.

America Lost Its Critical Mineral Independence. Washington Is Taking It Back.

A NASDAQ-Listed Royalty Vehicle Holds the Anchor Interest in What May Be One of the World’s Largest Undeveloped Critical Metals Projects

READ THE TMCR REGISTRATION STATEMENT HERE

Hello Everyone,

The company we are covering today is planting its flag in one of the most strategically important and consistently underfinanced sectors of the American economy.

Critical mineral security is creating what we see as the beginning of a potential structural realignment of American industrial capital.

When Washington decides a problem is a national security problem, capital flows. When one of the world's most reliable resource business models meets what we believe to be the most consequential resource category in decades, we see a structural opportunity. Not just for the companies developing the assets, but for the royalty vehicles structured to capture a percentage of everything that gets produced.

According to the US government and multiple federal agencies, the United States now depends on foreign sources, primarily China, for the majority of the critical minerals essential to modern defense, energy, and advanced technology. The materials used in F-35 fighter jets, electric vehicles, semiconductors, and grid-scale storage are predominantly controlled by strategic adversaries. Beijing's dominance of rare earth processing, nickel refining, and cobalt supply chains has given it strategic leverage over Western industry at a moment of historic geopolitical tension.

That problem cuts across every corner of the American industrial base. Defense, energy, transportation, advanced manufacturing, communications. All of it built on raw materials that the United States largely no longer controls.

Yet for all of that scale, the financing layer of the critical minerals industry is fundamentally underinvested. Royalty and streaming companies have delivered some of the most consistent outperformance in the mining sector over the past decade, with Franco-Nevada, Wheaton Precious Metals, and Royal Gold building their empires almost entirely on precious metals. Cumulative returns of more than 600% over the past decade. Trading at roughly 1.5–2.0x price-to-NAV versus approximately 0.7–1.0x for the diversified miners.

And yet, for all of the value the royalty model has created, we are unaware of anybodythat has applied it to critical minerals at scale.

Washington has now made critical mineral security a national priority, deploying executive authority, taking direct government equity stakes, and mobilizing institutional capital to reverse decades of supply chain vulnerability. Project Vault, a $12 billion domestic strategic critical minerals reserve. A $400 million Pentagon equity stake in MP Materials. A 10% government stake in Trilogy Metals. A 5% stake in Lithium Americas. $1.6 billion of backing for USA Rare Earth alone. The DFC joining a $1.8 billion consortium. JPMorganChase committing to a $1.5 trillion Security and Resiliency Initiative.

The forces behind every major resource cycle of the past two decades — the supply shock of OPEC dependence that unleashed the American shale boom, the China rare earth wake-up call, and now a coordinated federal push into onshoring — are converging on a category that has gone essentially untouched by the royalty majors.

What follows is a structural reset.

The company we are looking at today is endeavoring to occupy this white space. A purpose-built critical minerals royalty platform, anchored by a 2.0% gross overriding royalty on what may be one of the world's largest undeveloped polymetallic resources, currently with 66% strategic and insider ownership, and a free float below 20%.

A vehicle that does not build the mine. Does not run the workforce. Does not absorb rising fuel, labor, or capital costs. It simply holds a contractual right to a percentage of gross revenue from every nickel, copper, cobalt, and manganese unit produced and sold from the cornerstone asset, for the life of that asset.

Royalty rights on the NORI project. Strategic insider alignment from one of America's most consequential industrial families. A management team that has driven over C$5 billion in resource transactions. The critical minerals royalty category remains largely unaddressed by the established royalty majors. TMCR is a purpose-built vehicle attempting to fill that gap.

The Metals Royalty Company Inc. (NASDAQ: TMCR) is already operating inside that transformation.

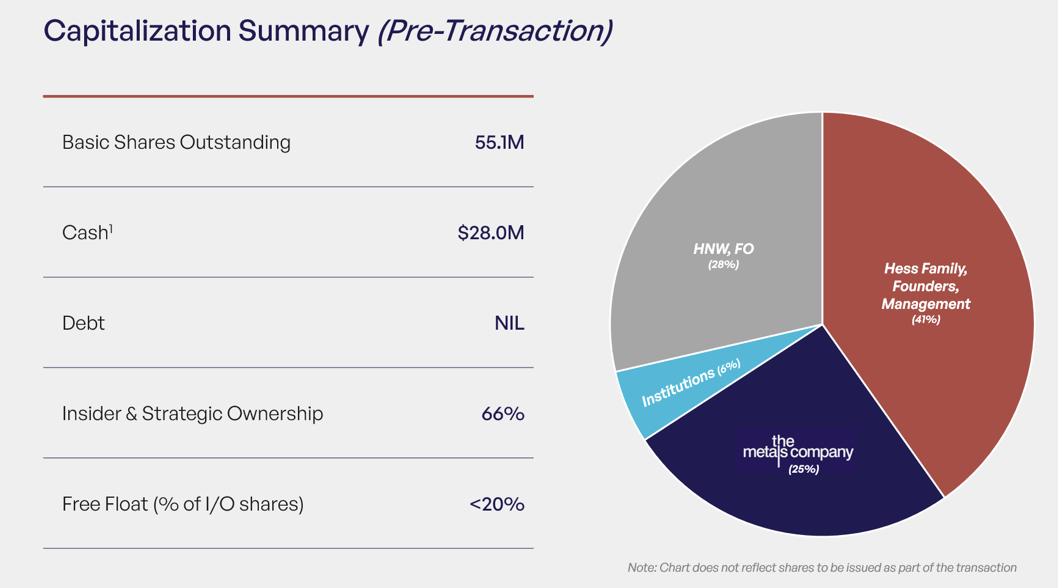

The company currently has approximately $28 million in cash and 55.1 million basic shares outstanding. Zero debt. ~66% strategic and insider ownership held by founders, management, the Hess family, and TMC the metals company itself. A free float of less than 20%. A 2.0% gross overriding royalty on the NORI concession, ranked by Mining.com as one of the world's potentially largest undeveloped nickel-equivalent resources. TMCR is converting structural advantages into real positioning at the precise moment the federal government is rewriting the playbook for American mineral security.

The royalty model has a long track record in precious metals — Franco-Nevada, Wheaton Precious Metals, and Royal Gold built multi-billion dollar platforms starting from single cornerstone assets. The Metals Royalty Company Inc. (NASDAQ: TMCR) is applying that same model to critical minerals, with a 2.0% gross overriding royalty already on the books and the regulatory pathway already moving.

TMCR has some major catalysts in play right now:

• Anchor Royalty on a Potentially Generational Critical Metals Asset: TMCR holds a 2.0% gross overriding royalty on all metals and minerals produced and sold from TMC the metals company's (NASDAQ: TMC) NORI concession in the Clarion-Clipperton Zone. Mining.com ranks NORI among the largest undeveloped nickel-equivalent resources on the planet — a polymetallic deposit of nickel, copper, cobalt, and manganese. The royalty is paid on top-line revenue, with no deductions for processing, refining, or operating costs.

• NOAA Issued a Full Compliance Determination on May 1, 2026: TMC USA's consolidated deep-seabed mining application — the first ever filed under the US Deep Seabed Hard Mineral Resources Act of 1980 — has now advanced into the certification stage, with TMC expecting a final permit decision before the end of Q1 2027. Every regulatory milestone between now and that decision narrows the remaining risk and increases the probability and proximity of TMCR’s paying, with no additional capital deployed by the company.

• $132.5 Million Mesabi Metallics Royalty Acquisition Announced May 6, 2026: TMCR has entered into a definitive agreement to acquire a 1.0% Index-Priced Gross Overriding Production Royalty on the Mesabi Metallics iron ore project in Nashwauk, Minnesota, one of the United States' few large-scale merchant DR-grade iron ore projects and a strategic input for the American green steel transition. First production is targeted for H2 2026, with anticipated initial annual royalty cash flow potential of up to ~$13M+ on production up to 8.5 Mtpa.The project is sponsored by Essar Group, approximately 93% complete, has a 23+ year mine life, and is backed by up to $10 billion of US Export-Import Bank support.

• Currently ~$28 Million in Cash and One of the Tightest Cap Tables We’ve Seen in the Sector: 55.1 million basic shares outstanding. Approximately 66% strategic and insider ownership across the Hess family, founders, management, and TMC. A public free float of less than 20%. There are no large blocks looking for the exit and no overhang from an early-stage financing that diluted the cap table.

• Hess Family Anchor Position: The Hess family, the American energy dynasty that sold Hess Corporation to Chevron for $55 billion in 2025, holds a cornerstone position in TMCR. Michael Hess, Chief Investment Officer of Hess Capital, serves as Strategic Advisor.

• Operator and Royalty Holder Are Structurally Aligned: TMC the metals company (NASDAQ: TMC), the operator of the NORI project, holds an approximately 25% strategic stake in TMCR. Gerard Barron, TMC's Co-Founder, Chairman and CEO, also sits on TMCR's board.

• First Production Targeted for Q4 2027: TMC has invested over $700 million and 15 years advancing NORI from concept toward commercial reality, including 23 offshore research campaigns, the first integrated nodule collection test since the 1970s, and the successful 2022 lift of more than 3,000 tonnes of nodules from the seafloor. Korea Zinc has invested $85.2 million as refining partner, Allseas serves as offshore partner and second-largest TMC shareholder, and Glencore has signed an offtake agreement covering 50% of expected nickel and copper production.

• A Decade of Demonstrated Outperformance From the Royalty Model: Per S&P Capital IQ and Bloomberg, the major royalty and streaming companies delivered cumulative returns of over 600% over the past decade and trade at roughly 2x P/NAV versus approximately 1x for the diversified miners. TMCR applies the most consistently outperforming business model in the natural resources sector to a category where the established royalty majors are not yet entrenched.

• The NORI Royalty Is the Anchor, Not the Ceiling: The mandate is to build a growing portfolio of royalties, streams, and structured interests across the full critical minerals value chain — from early exploration through production and mine expansion, across nickel, copper, cobalt, manganese, and adjacent minerals that define America's mineral security and re-industrialization challenge.

NOAA Advances NORI Application Into Certification Stage

Management Perspective

"I think we are living through the exact same moment as the shale revolution but in metals and mining. I have never seen capital flows like this. So it is definitely an exciting time to be in this space," said Brian Paes-Braga, Founder, Chairman and Chief Executive Officer of The Metals Royalty Company.

With NOAA's May 1, 2026 full compliance determination, the NORI consolidated application has now advanced into the certification stage. TMC expects a final permit decision before the end of Q1 2027. TMC the metals company is targeting first production in Q4 2027.

Operational and Financial Context

TMCR's royalty is structured as a gross overriding royalty (GORR), paid on a percentage of top-line gross revenue with no deductions for processing, refining, or operating costs. The company is not responsible for the construction or operation of the NORI project. If costs rise on the operator's side, TMCR's revenue is unaffected. When production scales, TMCR's revenue scales with the operator's gross revenue. Full upside participation. Zero direct cost exposure.

Subject to a buyback option of 1.5% with contracted IRRs reflective of project risk, the royalty covers all metals and minerals produced and sold from the NORI areas, for the life of the asset.

Liquidity and Capital Resources

TMCR entered the public market with approximately $28 million in cash. The capital structure is purpose-built as a permanent capital vehicle, without the constraints of short-term IRR mandates, and is designed to finance assets across full commodity cycles and hold them through the decades-long production profiles that world-class mining assets require.

Recent Developments

On January 26, 2026, TMC USA filed the first consolidated deep-seabed mining application under the US Deep Seabed Hard Mineral Resources Act of 1980. On March 9, 2026, NOAA determined the application was in substantial compliance with DSHMRA, advancing it into full technical and environmental review. On May 1, 2026, NOAA issued a full compliance determination, advancing the application into the certification stage.

The April 2025 executive order signed by President Trump directed federal agencies to accelerate the development of America's offshore and deep-sea critical mineral resources, citing national security and the need to reduce dependence on China. NOAA responded by accelerating its DSHMRA permitting timeline, giving TMC USA a US pathway to commercial recovery that does not rely on the United Nations' International Seabed Authority process. That independence matters. NORI is not subject to the multilateral delays that have stalled other deep-sea projects globally.

NORI Sits at the Top of a Resource Category That Is Almost Too Strategic to Ignore

The Metals Royalty Company Inc. (NASDAQ: TMCR) holds its anchor royalty on a deposit that Mining.com ranks as one of the world’s largest undeveloped nickel-equivalent resources on the planet. The Clarion-Clipperton Zone hosts polymetallic nodules that naturally concentrate the exact metals advanced economies need most: nickel, copper, cobalt, and manganese. Four of the most important inputs for EV batteries, grid storage, and defense applications. Rarely found together in one place. At NORI, they occur within each nodule.

The NORI concession covers approximately 74,830 km² of seabed in international waters between Hawaii and Mexico. Unlike conventional mining, there is no blasting, no tunneling, and no underground development. The collection technology was demonstrated at sea in 2022 by Allseas, lifting more than 3,000 tonnes of nodules from the seafloor in real-world conditions. Processing and refining work has been completed at pilot and bench scale through partnerships with Korea Zinc and PAMCO.

Critical mineral demand is a recurring industrial requirement that does not get cut when the economy softens. It is a national security obligation, an industrial input, and the foundation layer of the energy transition.

Management

Brian Paes-Braga – Founder, Chairman and CEO: Over a decade building, financing, and exiting growth-oriented resource and growth businesses, with over C$5 billion in transactions since 2015. Founder, Chairman and CEO of TMCR. Was a board member of DeepGreen Metals, now TMC the metals company Inc. (NASDAQ: TMC), from its earliest days. Helped build the foundation for the NORI project before founding the royalty vehicle to finance it.

Gerard Barron – Director (Non-Executive): Co-Founder, Chairman and CEO of TMC the metals company Inc. (NASDAQ: TMC), the operator of the NORI project on which TMCR's royalty sits. Has been building TMC since 2011, raised over $700 million to advance it, and oversees the regulatory and technical strategy that will determine the timing of first production. His seat on TMCR's board structurally aligns the operator and the royalty holder.

Michael Hess – Strategic Advisor: Chief Investment Officer of Hess Capital, the private and public investment arm of one of America's most consequential industrial families. Over 16 years evaluating and developing energy infrastructure businesses across the full investment cycle. Relationships across the American investment, policy, and industrial landscape that few advisors to a newly listed company can match.

Cornerstone Shareholders: Hess Family, Founders & Management (~41%) | TMC the metals company, NASDAQ: TMC (~25%) | HNW & Family Offices (~28%) | Institutions (~6%). Total strategic and insider ownership of approximately 66%. Public free float below 20%.

NEWS

May 1, 2026 – NOAA Issues Full Compliance Determination on TMC USA's Consolidated Deep-Seabed Mining Application

March 9, 2026 – NOAA Determines TMC USA's Consolidated Deep-Seabed Mining Application in Substantial Compliance With DSHMRA

January 2026 – TMC USA Files First Consolidated Deep-Seabed Mining Application Under DSHMRA

April 2025 – President Trump Signs Executive Order: Unleashing America's Offshore Critical Minerals and Resources

July 2025 – Pentagon Becomes Largest Shareholder in Rare Earth Magnet Maker MP Materials

September 2025 – US Government to Take 5% Stake in Lithium Americas Joint Venture With General Motors

— US Government to Take 10% Stake in Canadian Mining Company Trilogy Metals

February 2026 – Critical Minerals Ministerial: $12 Billion Project Vault Strategic Reserve

— DFC Joins $1.8 Billion Consortium to Secure Critical Mineral Supply Chains

— JPMorganChase Commits to $1.5 Trillion Multi-Year Security and Resiliency Initiative

— Mining.com: Ranking the World's Biggest Nickel Projects

Sincerely,

Notes

1 https://www.mining.com/featured-article/ranked-worlds-biggest-nickel-projects/

2 https://www.state.gov/releases/office-of-the-spokesperson/2026/02/2026-critical-minerals-ministerial

7 https://www.jpmorganchase.com/newsroom/press-releases/2025/jpmc-security-resiliency-initiative