SRFM

***** Sponsored by Surf Air Mobility (NYSE: SRFM)

Surf Air Mobility (NYSE: SRFM) Chairman, CEO, and Co-Founder Just Issued a Joint Letter to Shareholders Improving 2026 Adjusted EBITDA Guidance by Approximately 40%

Co-Founders, Officers, Directors, and Institutional Partners Are Putting $15 Million of Their Own Money Back Into the Company, Alongside $15 Million in Non-Dilutive Aircraft-Backed Credit

SurfOS Is Already Driving Measurable Results: 98% Q4 Completion Rate, Charter Revenue Up 36% YoY, and 29 Brokers Already Live on the Platform

READ THE FULL SHAREHOLDER LETTER HERE

___________________________________________

Hello Everyone,

Earlier this week, the Chairman of the Board, Chief Executive Officer, and Co-Founder of Surf Air Mobility (NYSE: SRFM) did something not often seen from a small-cap management team.

They signed a joint letter directly to shareholders, laid out exactly what is working, improvedguidance, and then put their own money back into the company.1

That is not a press release written by a PR firm. That is a statement of conviction from the people who built the business.

And the numbers behind it are what make this worth paying attention to.

Surf Air Mobility just improved its 2026 Adjusted EBITDA loss guidance by approximately 40%, from a prior range of $50 to $40 million down to a new range of $30 to $25 million for the full year. Revenue guidance was reaffirmed at $128 to $138 million for 2026, representing 20% to 30% growth over 2025.1

On the same day, the company announced $30 million in new capital structured to minimize dilution and execute on its 2026 plan. Fifteen million dollars in non-dilutive, aircraft-backed credit. And another fifteen million dollars in common equity, led by the co-founders with officers, directors, and existing institutional partners participating alongside.2

The message from management in the letter is direct. Quote:

"We are obtaining liquidity in the least dilutive manner and chose this path because we believe in the plan and are investing our own money behind it."1

The Shopify Comparison Explains Why This Matters

Most investors never heard of Shopify before it went public in 2015. But every time a merchant launched an online store, processed an order, or managed inventory at scale, Shopify was running the infrastructure behind the scenes. The company did not own a single warehouse. It did not sell a single product. It built the software infrastructure that hundreds of thousands of merchants depended on to run their entire businesses. Today that market cap sits above $120 billion.

You do not have to own the most stores. You have to own the operating layer that every store, or in this case, every operator, depends on.

Shopify proved it in e-commerce. Palantir proved it in defense intelligence. And right now, one publicly traded company is positioning itself to do the exact same thing for air mobility.

Regional aviation today looks like e-commerce did before Shopify came along. Fragmented. Broker dependent. Running on legacy systems. Operators make scheduling decisions on spreadsheets. Charter brokers spend hours sourcing aircraft that should take minutes. There is no unified platform tying any of it together.

That is the gap Surf Air Mobility (NYSE: SRFM) was built to fill. Not just as an airline, but as a platform company using its own network, which is one of the largest commuter airlines in the USby scheduled departures, as the real-world proving ground for its own technology.

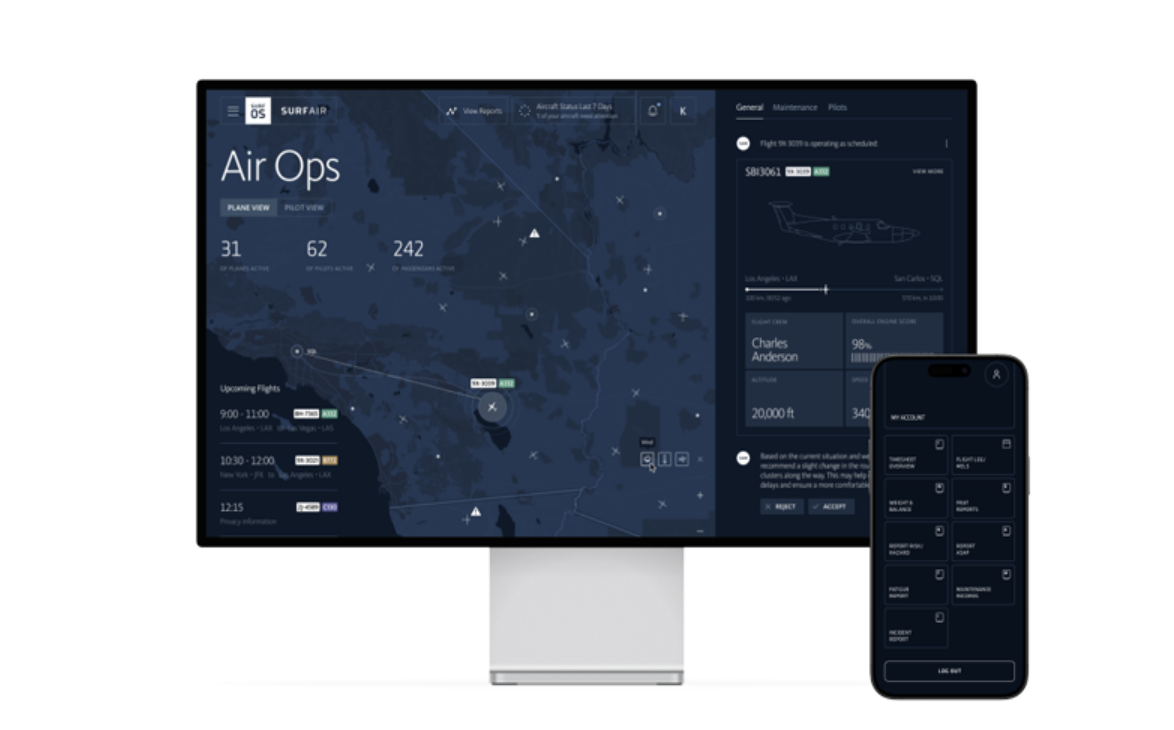

SurfOS Is No Longer a Pitch. It Is Already Producing Measurable Numbers.

Perhaps the most important section of today's shareholder letter is the one most small caps never get to write. The one where management shows that the software they have been talking about is already working.1

In 2025, Surf Air Mobility spent the year capturing data across its own operations and building SurfOS, the AI-enabled operating system powered by Palantir's AIP and Foundry platforms. In 2026, that investment is now showing up in the numbers.

Airline Operations (Southern Airways and Mokulele):

• Controllable completion rate hit 98% in Q4 20251

• On-time departures up more than 10 percentage points year-over-year1

• $1.3 million of incremental EBITDA expected this year from SurfOS-enabled improvements across crew, fleet, fuel utilization, spare parts discipline, and load factor optimization1

Surf On Demand Private Charter, the fastest-growing business:

• Q4 2025 charter revenue up over 36% year-over-year using BrokerOS1

• Powered by Surf On Demand program empowering independent brokers: six live, 23 in the pipeline, target of 100 by year-end1

• 32% more bookings for top brokers, 57% faster quote-to-close, and 40% more payments processed on the platform in Q1 2026 versus Q1 20251

Management put it plainly in the letter. Quote:

"The more data that flows through SurfOS, the smarter and more predictive it gets. That compounding advantage cannot be copied overnight and it is our moat."1

The SurfOS Commercialization Roadmap Is Already in Motion

BrokerOS (commercially launched December 2025): Independent brokers join the Powered by Surf On Demand program to sell under the Surf Air brand using SurfOS software. Surf Air Mobility takes a share of per-flight profit. 29 brokers are already enrolled, with hundreds of applicants in the queue.1

OperatorOS (launching second half of 2026): Small and mid-sized Part 135 operators integrate into the platform to optimize their operations. Management's target is 10 LOIs signed and five operators onboarded by year-end.1

SurfOS for Enterprise (active pipeline): Custom solutions for large operators, brokerages, and aircraft OEMs. Management is targeting multi-year, multi-million-dollar contracts this year. Through the exclusive teaming agreement with Palantir, Palantir's forward-deployed team is in every enterprise conversation.1

This is not a roadmap. It is a commercial pipeline with dates, targets, and a software product that is already in market generating revenue.

The Exclusive Palantir Partnership Is the Moat

Palantir Technologies (NASDAQ: PLTR) is the $350 billion AI company that built battlefield intelligence systems for the Pentagon and built data platforms used by US defense and public health agencies.

SRFM holds an exclusive five-year agreement with Palantir for the configuration and sale of Foundry and AIP-powered software to the Part 135 regional aviation market. No other company can offer this platform. That exclusivity is a structural moat.

Palantir is also one of the largest non-insider shareholders of Surf Air Mobility.3

And in October 2025, SRFM appointed Shawn Pelsinger to its board of directors.4 Pelsinger spent ten years as Global Head of Corporate Development and Senior Counsel at Palantir, where he personally helped build the Surf Air Mobility relationship. He also helped architect Skywise, the Palantir and Airbus partnership that became the data backbone for commercial aircraft maintenance globally.

Hawaii Is the Launchpad for Electric Aviation, Now at a Fraction of the Planned Cost

One of the most underappreciated lines in today's shareholder letter is this. Quote:

"Our strategic partnership with BETA Technologies allows us to capture the benefits of electrification at a fraction of the cost and at a faster pace. We have eliminated up to $100 million in planned Cessna Caravan electrification spend, significantly limiting potential dilution."1

That is a $100 million avoided capex number hidden inside an electrification strategy.

Through its Mokulele Airlines subsidiary, Surf Air Mobility (NYSE: SRFM) runs one of Hawaii's most extensive commuter networks. Nine airports. Ten routes. Over 224,000 passengers per year. Approximately 36,000 departures. A 97%-plus controllable completion factor. And an average stage length of 56 miles, the exact distance the first generation of commercial electric aircraft is being designed for.

On March 12, 2026, SRFM announced a strategic partnership with BETA Technologies to launch commercial electric aircraft service, starting in Hawaii.5 The deal includes a firm order for 25 electric aircraft, with options for up to 75 more. BETA's ALIA aircraft has already flown over 100,000 nautical miles in real-world operations.6

In 2026, BETA's electric aircraft will operate Mokulele cargo demonstration routes in Hawaii, laying the operational foundation for passenger service in the future.1

Surf Air Mobility has some major catalysts in play right now:

• Adjusted EBITDA Loss Guidance Improved ~40% for 2026: New guidance of $30 to $25 million in Adjusted EBITDA loss, down from the prior $50 to $40 million range. Revenue guidance reaffirmed at $128 to $138 million, representing 20-30% growth over 2025.1

• $30 Million in New Capital with Minimum Dilution: $15 million in non-dilutive, aircraft-backed credit. $15 million in common equity led by the co-founders, with officers, directors, and existing institutional partners participating. Management is investing its own money behind the plan.2

• SurfOS Is Helping Drive Measurable Results Inside the Business: Q4 2025 airline controllable completion rate of 98%. On-time departures up 10+ percentage points YoY. $1.3 million of incremental EBITDA expected this year from airline optimization. Charter revenue up 36% YoY in Q4 2025 using BrokerOS.1

• BrokerOS Is Already Live and Onboarding: The "Powered by Surf On Demand" program, which deploys BrokerOS to independent brokers, commercially launched in December 2025. Six brokers are already live on the platform, with 23 more in the pipeline and a stated target of 100 by year-end 2026. OperatorOS launches in the second half of 2026. Enterprise SurfOS contracts are in active pipeline via the exclusive Palantir teaming agreement. 1

• An Exclusive Palantir Partnership No Competitor Can Replicate: The five-year exclusivity agreement gives SRFM the sole right to configure and sell this software to the Part 135 regional aviation market. Palantir is one of the largest non-insider shareholders. The architect of the Palantir aviation playbook sits on the board.

• The Electrification Strategy Eliminated Up to $100M in Planned Capex: The BETA Technologies partnership locked in a firm order for 25 aircraft with options for 75 more. And Surf Air to eliminate up to $100 million in planned Cessna Caravan electrification program spending.1

• Real Revenue, Real Passengers, Real Operations: FY 2025 revenue of $106.6 million. 300,000+ passengers flew on more than 60,000 scheduled departures. Three consecutive quarters of positive Adjusted EBITDA in airline operations.7

• A $75 Billion to $115 Billion Market Opportunity: McKinsey projects the global regional air mobility market at $75 billion to $115 billion by 2035.8 NASA has called it transformational for American transportation. 5,000 underutilized regional airports. 90% of Americans within 30 minutes of one.9

While the Sector Burns Cash on Prototypes, One Company Is Already Flying

The advanced air mobility space has attracted billions in capital over the past five years. Most of it has gone to companies that have not yet carried a single paying passenger.

Surf Air Mobility (NYSE: SRFM) is operating in a different category entirely. FY 2025 revenue of $106.6 million. 300,000 passengers flown. SurfOS powered by Palantir, rolling out commercially, and producing measurable cost savings. BETA electric aircraft on firm order. Three consecutive quarters of profitable airline operations.

Compare that to the pure-play eVTOL names. Archer Aviation (NYSE: ACHR) remains effectively pre-revenue, with type certification still pending and its first commercial operations targeted for Abu Dhabi. Joby Aviation (NYSE: JOBY) generates revenue today, but only through its recent acquisition of Blade's helicopter and seaplane passenger business, while its own eVTOL air taxi service has yet to carry a paying passenger and is targeted for a Dubai launch in 2026. SkyWest (NASDAQ: SKYW) operates at massive scale as a regional feeder airline, but has no AI software platform and no electrification pathway.

The point is not that the competitors are bad companies. The point is that SRFM is the only company in the space simultaneously generating real revenue from its own scheduled operations, commercializing an AI-enabled software platform for the industry, pursuing electrification with a live aircraft order, and trading at a fraction of the valuation its pre-revenue eVTOL peers command.

The Smart Money Is Already Here

When the co-founders and officers put their own capital back into the company alongside institutional partners, that is conviction.2 When the architect of Palantir's aviation strategy joins the board of directors, that is a third.

The broader institutional shareholder base at SRFM includes Palantir Technologies (NASDAQ: PLTR), Vanguard, Raymond James, BlackRock, Rathbone, and Colony Group.These are not retail speculators chasing a headline.10

HC Wainwright has initiated coverage of Surf Air Mobility (NYSE: SRFM) with a Buy rating. CEO Deanna White and CFO Oliver Reeves have presented at the HC Wainwright AeroNext Conference and the Needham Industrial Tech Conference.

The Team That Has Already Built This Before

Great technology and great timing mean nothing without a team that knows how to execute inside a regulated industry. Airline licenses, STC certifications, and Palantir partnerships go to companies that execute. The leadership of SRFM is not a group of first-time founders learning on the job.

Carl Albert, Chairman of the Board. Deep aviation industry experience. Former principal investor and Chairman and CEO of Wings West Airlines, a regional airline operating as American Eagle that was acquired by AMR, the parent of American Airlines. Former Chairman and CEO of Fairchild Aircraft for ten years, where Fairchild acquired German aircraft manufacturer Dornier Luftfahrt. Decades of experience shepherding aircraft Type Certificates and Supplemental Type Certificates through the FAA, EASA, and other global authorities.

Deanna White, Chief Executive Officer. Over 20 years in aerospace. Former CFO of Surf Air, COO of Kitty Hawk, the Larry Page-backed eVTOL company whose aircraft program was sold to Boeing and rebranded as Wisk Aero, and former CEO of Bombardier Flexjet, the fractional jet ownership business later acquired by Directional Aviation Capital and built into one of the largest private aviation companies in the world.

Sudhin Shahani, Co-Founder. Co-founded Surf Air in 2013. Has led multiple rounds of capital formation across the company's history and been central to its Palantir and Textron strategic partnerships. He put $1 million back into the company in the November 2025 transaction and is supporting the $15 million co-founder-led equity round announced this week. That is called conviction.

Oliver Reeves, Chief Financial Officer. Over a decade in capital markets, software, and financial strategy. Previously Chief Strategy Officer at Xinuos. Columbia MBA.

Shawn Pelsinger, Board of Directors. Ten years as Global Head of Corporate Development and Senior Counsel at Palantir. Personally built the Surf Air relationship. Architected Skywise, the Palantir and Airbus aviation data platform that became the global standard for commercial aircraft maintenance. Currently Chief Administrative Officer and Chief Legal Officer at Acrisure.

What to Watch in 2026

Today's shareholder letter laid out the exact milestones the company is holding itself to for the rest of 2026. These are the checkpoints:

• Continued digitalization and optimization of airline operations

• Surf On Demand private charter revenue and margin expansion

• 100 brokers onboarded to the Powered by Surf On Demand program

• 10 OperatorOS LOIs signed, with 5 operators live

• First SurfOS Enterprise contracts signed

• BETA electric cargo demonstration flights in Hawaii

Management wrote it plainly. Quote:

"The software is live. The partners are committed. Our own capital is in this round. And the operating numbers are moving in the right direction."1

The Setup in Plain Terms

• 2026 Adjusted EBITDA loss guidance improved ~40%, from $50-$40M loss to $30-$25M loss

• 2026 revenue guidance reaffirmed at $128-$138 million, 20-30% growth over 2025

• $30 million in new capital announced this week: $15M non-dilutive aircraft-backed credit plus $15M co-founder-led equity

• BrokerOS commercially launched December 2025 with 6 brokers live and 23 more in the pipeline

• Q4 2025 airline controllable completion rate of 98% and on-time departures up 10+ points YoY

• Q4 2025 Surf On Demand charter revenue up 36% YoY via BrokerOS

• Exclusive five-year Palantir agreement for Part 135 aviation software

• Up to $100M in planned Caravan electrification spend eliminated

• 25 BETA electric aircraft on firm order, options for 75 more

• FY 2025 revenue of $106.6M and full-year airline operations profitability on an Adjusted EBITDA basis

• Palantir is one of the largest outside shareholders; other institutional holders include Vanguard, BlackRock, Raymond James, Rathbone, and Colony Group

• HC Wainwright Buy rating with $12 price target

• A $75 billion to $115 billion regional air mobility market opportunity by 2035

Real planes. Real passengers. Real revenue. Real software. Insider capital going back in. Guidance moving up, not down.

That is the Surf Air Mobility (NYSE: SRFM) story today. And it is just getting started.

Remember to do your own research.

Sincerely,

Notes

9 https://www.nasa.gov/aeronautics/regional-air-mobility/

10 https://fintel.io/so/us/srfm

DISCLAIMER

THIS WEBSITE/NEWSLETTER IS A PUBLICATION OF ONE22 MEDIA, LLC, HEREIN REFERRED TO AS O22. O22’S REPORTS/RELEASES ARE A COMMERCIAL ADVERTISEMENT AND ARE FOR GENERAL INFORMATIONAL PURPOSES ONLY.O22 IS ENGAGED IN THE BUSINESS OF MARKETING AND ADVERTISING COMPANIES FOR MONETARY COMPENSATION.

O22 HAS BEEN COMPENSATED A FEE OF TWENTY THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 4/21/26. O22 HAS BEEN COMPENSATED A FEE OF TWENTY THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 3/20/26. O22 HAS PREVIOUSLY BEEN COMPENSATED A FEE OF FIFTEEN THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 2/6/26. O22 HAS PREVIOUSLY BEEN COMPENSATED A FEE OF TWENTY THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 11/6/25. O22 HAS BEEN COMPENSATED A FEE OF TWENTY THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 8/28/25. O22 HAS PREVIOUSLY BEEN COMPENSATED A FEE OF TWENTY THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 7/14/25. O22 HAS PREVIOUSLY BEEN COMPENSATED A FEE OF TWENTY THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 6/1/25. O22 HAS BEEN COMPENSATED A FEE OF TWELVE THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE BEGINNING ON 1/28/25. O22 HAS PREVIOUSLY BEEN COMPENSATED A FEE OF SEVEN THOUSAND FIVE HUNDRED USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE. O22 HAS PREVIOUSLY BEEN COMPENSATED A FEE OF TWENTY TWO THOUSAND USD BY A THIRD PARTY, LFG EQUITIES CORP FOR A ONE DAY SRFM PROFILE.

BY SUBSCRIBING TO OR OTHERWISE USING THIS WEBSITE/NEWSLETTER, YOU AGREE TO HOLD O22 AND ITS OPERATORS, OWNERS, AND EMPLOYEES HARMLESS AND TO COMPLETELY RELEASE THEM FROM ANY AND ALL LIABILITY DUE TO ANY AND ALL LOSS, DAMAGE, OR INJURY THAT YOU MAY INCUR, MONETARY OR OTHERWISE.

INVESTING IN MICRO-CAP AND GROWTH SECURITIES IS HIGHLY SPECULATIVE AND CARRIES AN EXTREMELY HIGH DEGREE OF RISK. NEVER INVEST IN ANY STOCK FEATURED ON O22’S SITE OR NEWSLETTER UNLESS YOU CAN AFFORD TO LOSE YOUR ENTIRE INVESTMENT. THE DISCLAIMER IS TO BE READ AND FULLY UNDERSTOOD BEFORE USING O22’S SERVICES, JOINING O22’S SITE OR EMAIL/BLOG LIST, OR FOLLOWING ANY SOCIAL NETWORKING PLATFORMS O22 MAY USE.

PLEASE NOTE WELL: O22 IS NOT A REGISTERED INVESTMENT ADVISOR, BROKER DEALER OR A MEMBER OF ANY ASSOCIATION FOR OTHER RESEARCH PROVIDERS IN ANY JURISDICTION WHATSOEVER. O22 IS NOT AFFILIATED WITH ANY EXCHANGE, ELECTRONIC QUOTATION SYSTEM, THE SECURITIES AND EXCHANGE COMMISSION, OR FINRA. NONE OF THE MATERIALS OR ADVERTISEMENTS HEREIN CONSTITUTE OFFERS OR SOLICITATIONS TO PURCHASE OR SELL SECURITIES OF THE COMPANIES PROFILED.

THE INFORMATION CONTAINED HEREIN IS BASED ON INFORMATION SUPPLIED BY THE COMPANIES PROFILED, PUBLICLY AVAILABLE INFORMATION, PRESS RELEASES, AND OTHER SOURCES WHICH O22 BELIEVES TO BE RELIABLE, BUT IS NOT GUARANTEED BY O22 AS BEING ACCURATE AND DOES NOT PURPORT TO BE A COMPLETE STATEMENT OR SUMMARY OF THE AVAILABLE DATA. O22 IS NOT RESPONSIBLE FOR ANY CLAIMS MADE BY THE COMPANIES PROFILED. INVESTORS SHOULD NOT RELY ON THE INFORMATION CONTAINED IN THIS WEBSITE/NEWSLETTER IN DECIDING TO INVEST OR MAKE OTHER FINANCIAL DECISIONS. RATHER, INVESTORS SHOULD USE THE INFORMATION CONTAINED IN THIS WEBSITE/NEWSLETTER AS A STARTING POINT FOR DOING ADDITIONAL INDEPENDENT RESEARCH ON THE FEATURED COMPANIES. O22 STRONGLY ENCOURAGES READERS AND INVESTORS TO CONDUCT A COMPLETE AND INDEPENDENT INVESTIGATION OF THE RESPECTIVE COMPANIES, INCLUDING BY REVIEWING SEC FILINGS (FORMS 10-Q, 10-K, 8-K, 3, 4, 5, SCHEDULE 13D) AND BY CONSULTING YOUR OWN TAX, BUSINESS, FINANCIAL, AND INVESTMENT ADVISORS.

THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995 PROVIDES A SAFE HARBOR IN REGARD TO FORWARD-LOOKING STATEMENTS. ANY STATEMENTS THAT EXPRESS OR INVOLVE DISCUSSIONS WITH RESPECT TO PREDICTIONS, EXPECTATIONS, BELIEFS, PLANS, PROJECTIONS, OBJECTIVES, GOALS, ASSUMPTIONS OR FUTURE EVENTS OR PERFORMANCE ARE NOT STATEMENTS OF HISTORICAL FACT, AND MAY BE FORWARD-LOOKING STATEMENTS. FORWARD-LOOKING STATEMENTS ARE BASED ON EXPECTATIONS, ESTIMATES, AND PROJECTIONS AT THE TIME THE STATEMENTS ARE MADE THAT INVOLVE A NUMBER OF RISKS AND UNCERTAINTIES WHICH COULD CAUSE ACTUAL RESULTS OR EVENTS TO DIFFER MATERIALLY FROM THOSE PRESENTLY ANTICIPATED. FORWARD-LOOKING STATEMENTS MAY BE IDENTIFIED THROUGH USE OF WORDS SUCH AS PROJECTS, FORESEES, EXPECTS, ANTICIPATES, ESTIMATES, BELIEVES, UNDERSTANDS, MAY, COULD, OR MIGHT. THERE IS NO GUARANTEE THAT PAST PERFORMANCE WILL BE INDICATIVE OF FUTURE RESULTS.